NSFI 2025–30 Expands Role of Fintechs, Skill Providers, and Community Institutions

Financial Inclusion is the process of ensuring access to financial services, timely and adequate credit for vulnerable groups such as weaker sections and low-income groups at an affordable cost.

The FI ecosystem focuses on enhancing four key wellbeing parameters—financial safety, financial security, financial resilience, and financial discipline.

“Financial inclusion is the cornerstone for equitable economic development.” – Sanjay Malhotra, RBI Governor – December 1, 2025

The National Strategy for Financial Inclusion (NSFI) 2025–30, approved by the Sub-Committee of the Financial Stability and Development Council (FSDC-SC) in its 32nd meeting, was officially released bySanjay Malhotra, Governor, Reserve Bank of India, on December 1, 2025, in Mumbai. The previous five-year strategy, NSFI 2019–24, brought notable improvements across access, usage, and quality dimensions of financial inclusion. The new strategy aims to consolidate these advancements while pushing the boundaries further to achieve deeper, more resilient, and sustainable financial inclusion outcomes.

A Synergistic Approach to Deepen Financial Inclusion

The NSFI 2025–30 underscores a synergistic ecosystem approach, aimed at strengthening the quality and consistency of last-mile access and enhancing the effective usage of formal financial services across the country.

The Strategy outlines five strategic pillars, collectively termed as ‘Panch-Jyoti’, supported by a menu of 47 actionable points. These pillars aim to elevate the state of financial inclusion for households and micro-enterprises.

The Five Pillars of ‘Panch-Jyoti’

- Equitable, Responsible, Suitable, and Affordable Financial Services

Enhancing access to a comprehensive bouquet of financial services to promote financial safety and financial security for households and micro enterprises. - Gender-Sensitive and Differentiated Inclusion Approach

Designing women-led financial inclusion models and targeted strategies to improve financial resilience, especially for underserved and vulnerable segments. - Synergy Between Livelihood, Skill Development, and Financial Inclusion

Strengthening linkages between financial services, livelihood enablers, and skilling institutions to reinforce sustainable economic opportunities. - Financial Education for Building Financial Discipline

Positioning financial education as a transformative tool to promote informed financial decision-making and long-term financial wellbeing. - Robust Customer Protection and Grievance Redressal

Enhancing the quality, speed, and reliability of customer protection frameworks to build trust and ensure fair outcomes.

Built on Extensive Nationwide Consultations

The Strategy has been framed under the guidance of the Technical Group on Financial Inclusion and Financial Literacy (TGFIFL). It is the result of nationwide discussions conducted by the RBI with diverse stakeholders, and consultations with:

- Department of Economic Affairs

- Department of Financial Services, Ministry of Finance

- Securities and Exchange Board of India

- Insurance Regulatory and Development Authority of India

- Pension Fund Regulatory and Development Authority

- National Bank for Agriculture and Rural Development

- National Skill Development Corporation

- National Centre for Financial Education

Vision of National Strategy for Financial Inclusion (NSFI) 2025-30

An inclusive financial system for the well-being of people

Financial inclusion initiatives generally begin with supply initiatives to provide affordable, easy, trusted, and fair access to regulated financial services, namely, savings, payments, investments, credit, remittances, insurance, and pension to hitherto excluded and marginalized segments of society. Though financial inclusion falls within the ambit of the financial sector, financial inclusion policies have far and wide positive impacts and correlations in the socioeconomic domain.

Financial inclusion is referred in the targets of eight out of the seventeen United Nations Sustainable Development Goals (SDGs)12, namely, SDG-1 on eradicating poverty, SDG-2 on ending hunger, achieving food security, and promoting sustainable agriculture, SDG-3 on promoting health and well-being, SDG-5 on achieving gender equality and economic empowerment of women, SDG-8 on promoting economic growth and jobs, SDG-9 on supporting industry, innovation and infrastructure, SDG-10 on reducing inequality, and SDG-17 on strengthening the means of implementation (Table III.1).

Financial inclusion, being an aspirational journey, starts from creating opportunities for access to the formal financial system for the hitherto excluded and underserved segments, but its mandate goes beyond access to ensure effective usage of financial services to the benefit of people. Effective usage requires that people have an economic case for using the formal financial services, which primarily comes from their capacity to have regular income/cash flow through employment, livelihood, etc., and have a perceptible economic incentive for using formal financial services.

The sustenance and growth of usage also require continued trust of the people, suitability of products and services, sound financial literacy, a pro-active/quick grievance redressal mechanism, and a positive perception of being heard, which are some of the quality aspects of financial inclusion.

Seen in the above context and in accordance with the role of financial inclusion in the achievement of sustainable development goals, it is obvious that financial inclusion is not just an end in itself but a means to a greater end of ensuring the overall well-being of people.

Table III.1: Role of FI Policies in Specific SDGs and Targets

SDG 1: Poverty Reduction

Financial inclusion by improving access to financial services and skilling/livelihood opportunities helps to improve the sustenance, sufficiency, and safety of income, thereby helping to reduce poverty.

SDG 2: Ending Hunger

An inclusive financial system incentivises credit-led investments for adoption of sustainable and productivity-enhancing agricultural practices, which results in better agricultural yields. Thereby, helping in reducing hunger due to enhanced food security.

SDG 3: Health and Wellbeing

Financial inclusion through its multi-faceted socio-economic dimensions aids human development and augments resilience of the marginalised and vulnerable, thereby fostering health and well-being.

SDG 5: Gender Equality

Gender-sensitive financial inclusion policies decrease gender inequality by empowering women and improving their overall socio-economic status.

SDG 8: Decent Work and Economic Growth

Financial inclusion with its ecosystem approach supports economic growth by providing necessary funding, augmenting employment, and entrepreneurship, and boosting consumption.

SDG 9: Industry, Innovation, and Infrastructure

Financial inclusion policies support the industry, especially the micro and small enterprises, by providing credit linkages and digital infrastructure for promoting innovation and boosting their progress.

SDG 10: Reducing Inequalities

Financial inclusion policies with their specific focus on the upliftment of the poor, marginalised, and vulnerable segments, and the last mile reach, help to reduce inequalities.

SDG 17: Strengthening the Means of Implementation

Financial inclusion is an important means of implementation for achieving SDGs, through mobilization of savings/investments and boosting consumption, and improving overall wellbeing of people, that can help in achieving broader developmental goals.

Definition of Financial Inclusion

The Committee on Financial Inclusion (Chairman: Dr C Rangarajan, RBI, 2008) defined financial inclusion as “the process of ensuring access to financial services, timely and adequate credit for vulnerable groups such as weaker sections and low-income groups at an affordable cost”.

Further, the Committee on Medium-Term Path to Financial Inclusion (Chairman: Shri Deepak Mohanty, RBI, 2015) viewed financial inclusion as, “convenient access to a basket of basic formal financial products and services that should include savings, remittance, credit, government-supported insurance and pension products to small and marginal farmers and low-income households at reasonable cost with adequate protection progressively supplemented by social cash transfers, besides increasing the access of small and marginal enterprises to formal finance with a greater reliance on technology to cut costs and improve service delivery.”

The NSFI (2019–24) aimed at broadening, deepening, and accelerating financial inclusion alongside promoting financial literacy and consumer protection, with a view to promoting economic wellbeing, prosperity, and sustainable development.

Continuing the journey and leveraging the substantial gains during the last decade in the bank account ownership to near saturation, robust expansion in physical and digital access infrastructure, and improvements in customer awareness and protection measures, it is desirable to upscale the focus of financial inclusion by adopting a synergistic ecosystem approach. This would ensure integrated and seamless involvement of stakeholders for developing a truly inclusive financial system towards wellbeing of people by minimization of inequality of opportunities for people to reap the benefits of access to formal financial system, while substantially improving the quality and consistency of last mile reach.

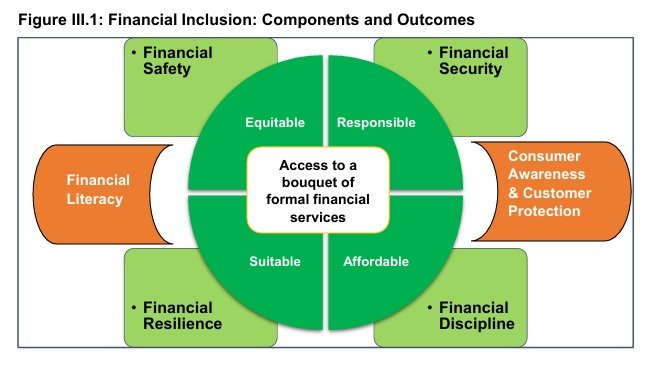

Financial inclusion policies duly integrated with livelihood support, market linkages, financial education, and customer protection initiatives are great enablers of an improved state of the economic wellbeing of people. Pursued holistically, financial inclusion can lead to desirable outcomes in form of a quadrangle of financial safety, financial security, financial resilience, and financial discipline, in turn contributing towards overall wellbeing of people.

The objective of Financial Inclusion

The objective of Financial Inclusion is ensuring availability of equitable, responsible, suitable, and affordable access to a bouquet of formal financial services, namely, savings, payments, remittances, credit, investments, insurance, and pension, across socio-economic and geographical strata, coupled with effective financial literacy, robust consumer awareness and customer protection measures.

Financial inclusion, as above, with the involvement of all stakeholders, improves financial safety, financial security, financial resilience, and financial discipline of individuals (households) and micro-enterprises.

Hence, the objectives and intended outcome of financial inclusion to be pursued under NSFI: 2025–30 are presented below. Figure 1 provides a diagrammatic presentation of the components and outcomes of financial inclusion.

To explain, the usage of terms regarding access to a bouquet of financial services in the above definition would generally mean the following –

a. Equitable – The access infrastructure should be available across the geographic strata in a reasonably homogeneous manner.

b. Responsible – The financial service providers should ensure that their products/ services do not manipulate or impede customers’ free choices, interests, and right to product suitability, and do not leave customers’ worse off in terms of the economic, behavioural, and social outcomes.

c. Suitable – Financial products and services should be appropriate to customers need and based on customers’ financial circumstances and understanding. Differentiated/customised services should be available to enable people to choose what is best for them.

d. Affordable – The basic minimum financial services (basic transaction account, basic savings and investment account, small value remittances, small value digital payments, etc.) should be offered free of cost. Pricing of other services should have an essential element of affordability, keeping in mind the marginal cost of services.

Table.1: The Quadrangle of Financial Safety, Security, Resilience, and Discipline and Their Anchors

| Dimension | Anchors | Explanatory Details on Anchors |

|---|---|---|

| Financial Safety – “Smoothly managing day-to-day transactions” | – Suitable Access – Livelihood Support – Customer Protection | – Fair, suitable, and affordable financial products and services. – Quick, simple, and efficient grievance redressal mechanism. – Regular and sustained income stream through wage or non-wage livelihood. – Meeting basic subsistence needs (food, shelter, education, travel, etc.) at a household level. |

| Financial Security – “Ability to meet any contingency” | – Regular Savings – Pension Subscription – Customer Protection Measures | – Regular savings—liquid (for at least two months’ average household expenses) and long-term (physical/financial assets). – Continued subscription to pension schemes (retirement pension / Atal Pension Yojana / other social security pensions). – Effective ex ante customer protection measures and deposit insurance. |

| Financial Resilience – “Ability to recover from financial setbacks” | – Insurance Coverage – Credit Facilities | – Unexpired insurance coverage at acceptable cost—life, health, and asset insurance (vehicles, property, machinery). – Fair emergency credit to cope with financial setbacks such as loss of life, livelihood, or assets, without excessive debt burden or disruption to daily life. |

| Financial Discipline – “Attitude and behaviour towards a steady financial future” | – Financial Education – Experiential Learning | – Financial awareness and confidence. – Diversified investments across different banks/asset classes. – Sustainable indebtedness—monthly loan repayment not exceeding half of the household’s monthly income. – Realistic goal setting and planning for future expenses and life events (education, marriage of children, retirement, etc.). |

Financial Inclusion (FI) Ecosystem

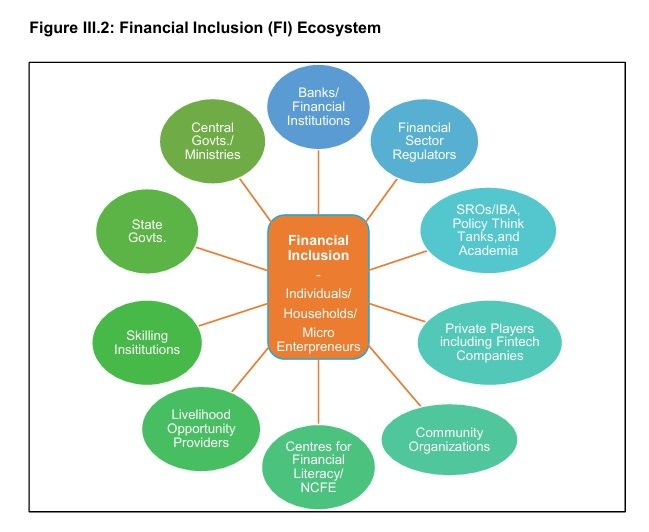

As already discussed, an ecosystem approach to financial inclusion is required for ensuring an integrated and synergistic involvement of stakeholders for the effectiveness of financial inclusion initiatives and outcomes. Hence, a clear understanding and definition of the financial inclusion (FI) ecosystem would be helpful for seamless coordination towards achieving the shared goals.

The FI ecosystem refers to a synergised network of stakeholders working and/or connected with financial inclusion initiatives and their outcomes in the form of the wellbeing of people—represented through the quadrangle of financial safety, security, resilience, and discipline. Seamless and well-coordinated functioning of the ecosystem, comprising stakeholders such as banks and financial institutions including NABARD and SIDBI, the central and state governments, financial sector regulators, SROs/IBA, private players including fintech companies, think tanks, academia, community organizations, Centres for Financial Literacy and NCFE, livelihood opportunity providers13, and skilling institutions, is essential for effective and outcome-oriented financial inclusion policies (Figure 2).

Vision of NSFI (2025–30)

“To strengthen the financial inclusion ecosystem with the synergised efforts of stakeholders towards wellbeing of people by ensuring delivery of equitable, responsible, suitable, and affordable financial services duly supported by livelihood enablers, effective financial literacy, digital public infrastructure, and robust customer protection.”

The current iteration of the National Strategy for Financial Inclusion for the period 2025–30 (NSFI: 2025–30) is an outcome of wide-ranging stakeholder consultations. The strategy is informed by the achievements of NSFI 2019–24 and focuses on further deepening, sustaining, and synergising financial inclusion initiatives.

©ambedkarchamber.com

{kind=link}