MSME credit rises to ₹31.09 lakh crore in FY25, growth slows to 14.1%; Small Finance Banks lead with 35.6%.

MUMBAI: Bank lending to micro, small and medium enterprises (MSMEs) continued to increase in 2024-25, but the pace of growth slowed compared to the previous year, according to the latest Reserve Bank of India (RBI) data “Report on Trend and Progress of Banking in India 2024-25”. At the same time, Small Finance Banks (SFBs) sharply expanded lending, while digital systems such as TReDS and ULI quietly helped smaller firms access credit faster.

Overall MSME credit still rising, but momentum weakens

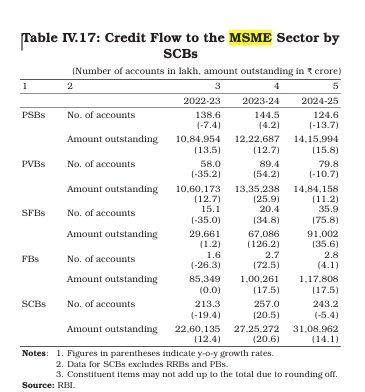

Total MSME credit from Scheduled Commercial Banks (SCBs) rose to ₹31.09 lakh crore by the end of March 2025. This means banks are still lending more money to small businesses. However, the growth rate slowed to 14.1% in FY25, compared to 20.6% in FY24, showing that banks are becoming more cautious.

MSMEs’ share in bank lending slightly declines

MSME loans made up 19.0% of total adjusted bank credit at end-March 2025, slightly lower than 19.3% a year earlier. In simple terms, MSMEs are still an important part of bank lending, but their share is no longer increasing as fast as before.

Small Finance Banks lead MSME lending growth

Among all bank groups, Small Finance Banks recorded the fastest growth in MSME lending during 2024-25. Their MSME credit grew by 35.6%, far higher than other banks. This suggests SFBs are actively lending to smaller businesses, especially in semi-urban and rural areas where access to credit is limited.

Summary of Growth Rates (2024-25)

| Bank Category | Growth in No. of Accounts | Growth in Amount Outstanding |

| Public Sector Banks | -13.7% (Negative) | 15.8% (Positive) |

| Private Sector Banks | -10.7% (Negative) | 11.2% (Positive) |

| Small Finance Banks | 75.8% (Positive) | 35.6% (Positive) |

| Foreign Banks | 4.1% (Positive) | 17.5% (Positive) |

| Total SCBs | -5.4% (Negative) | 14.1% (Positive) |

Public and private banks show slower pace

Foreign banks grew MSME lending by 17.5%, while public sector banks posted 15.8% growth. Private sector banks recorded the slowest growth at 11.2%. This indicates that large private banks, after aggressive lending earlier, have slowed down in FY25.

Fewer MSME loan accounts, but more money per borrower

Even though MSME credit increased, the number of MSME loan accounts fell by 5.4% across all SCBs in 2024-25. This means banks are giving bigger loans to fewer borrowers, rather than adding many new MSME customers.

Small Finance Banks add borrowers aggressively

SFBs were again different from other banks. Their MSME loan accounts jumped by 75.8%, showing that they are actively onboarding new small business borrowers. This makes SFBs a key lender for first-time or very small entrepreneurs.

Public sector banks reduce MSME accounts sharply

Public sector banks saw a 13.7% fall in MSME loan accounts in FY25. After a small recovery in FY24, the number of borrowers dropped sharply again. This suggests government banks are tightening lending standards or focusing on select borrowers.

Despite fewer accounts, PSBs lend more money

Even with fewer MSME loan accounts, public sector banks increased MSME credit outstanding to ₹14.16 lakh crore, registering 15.8% growth. In simple words, PSBs lent more money, but to a smaller group of MSMEs.

Medium enterprises get more credit than smaller units

Within MSMEs, medium-sized enterprises saw stronger credit growth than micro and small units. Credit to micro and small industries grew by 8.9%, while medium enterprises recorded 18.5% growth. Banks appear more comfortable lending to relatively stable and larger MSMEs.

NBFCs step in where banks slow down

Non-banking financial companies (NBFCs) continued to expand their role in MSME lending. By March 2025, MSME loans accounted for nearly 10% of total NBFC credit. NBFCs often offer faster approvals and customised products, especially for service businesses like traders, transporters, and small service firms.

TReDS helps MSMEs convert invoices into cash

The Trade Receivables Discounting System (TReDS) saw strong growth in FY25. More MSMEs used the platform to get early payment against invoices raised on large buyers. The success rate improved to 95.3%, meaning most invoices uploaded were successfully financed.

ULI aims to speed up digital lending

The Unified Lending Interface (ULI) is being developed as a digital backbone for lending. It allows banks and lenders to access verified data and make quicker credit decisions. Unsecured MSME loans are among the supported categories, helping reduce paperwork and approval time.

Asset quality improves, but small units still under stress

Overall asset quality in priority sector lending improved, with the gross NPA ratio falling to 4.0% by March 2025. However, micro and small enterprises still contribute a large share of stressed loans, especially in public sector banks.

Smaller MSMEs show higher stress than medium units

In NBFCs, gross NPAs for micro and small industrial units stood at 5.4%, compared to 3.0% for medium enterprises. This higher stress is one reason lenders remain cautious while lending to very small businesses.

Priority sector targets met for micro enterprises

Banks exceeded the RBI’s micro-enterprise lending target. By March 2025, micro enterprise loans reached ₹13.89 lakh crore, equal to 9.2% of adjusted bank credit, well above the 7.5% requirement.

Regulatory changes affect MSME borrowers

RBI rules now offer more flexibility to MSMEs. Many floating-rate MSME loans do not attract pre-payment penalties. Voluntary gold or silver collateral within limits is allowed. However, proposed Basel III changes may make banks more selective in future.

What this means for MSME owners

Credit is still available, but banks are more careful. Small Finance Banks and NBFCs may remain easier options for smaller loans. Using digital platforms, maintaining GST records, and keeping clean bank statements will increasingly decide who gets loans.

Impact on jobs and local economies

MSME credit supports salaries, inventory, and local supply chains. Slower growth may affect job creation, but continued lending still helps sustain economic activity, especially outside big cities.

Risk remains, despite digital push

While digital lending is expanding, risks remain from cyber issues and repayment stress among micro units. As a result, lenders are likely to tighten checks even as technology speeds up approvals.

==

Micro, Small, and Medium Enterprises (MSME) are a cornerstone of the Indian financial and economic system

The Micro, Small, and Medium Enterprises (MSME) sector remains a cornerstone of the Indian financial and economic system, serving as a critical driver of growth and financial inclusion. According to the sources, the Reserve Bank of India (RBI) and the Central Government prioritize credit flow to this sector to meet the financing needs of a growing economy. MSMEs are categorized as productive sectors that support underserved populations, and regulatory policies are continually aligned to enhance their resilience and competitiveness.

Credit Flow and Deployment Dynamics

Credit to the MSME sector is provided by various regulated entities, including Scheduled Commercial Banks (SCBs) and Non-Banking Financial Companies (NBFCs).

Performance of Scheduled Commercial Banks (SCBs)

The growth of credit to the MSME sector by SCBs decelerated during 2024-25, though it continued to remain in double digits. By the end of March 2025, MSME credit as a proportion of total adjusted net bank credit stood at 19.0 per cent. Public Sector Banks (PSBs) saw an acceleration in credit growth to MSMEs, reaching an amount outstanding of ₹14,15,994 crore, while Private Sector Banks (PVBs) recorded a moderation at ₹14,84,158 crore. Small Finance Banks (SFBs) showed significant expansion, with their number of MSME accounts increasing by 75.8 per cent in the 2024-25 period.

Industrial Breakdown of Credit

Within the industrial sector, medium industries experienced an acceleration in credit growth during 2024-25. In contrast, micro and small industries, along with large industries, recorded a deceleration. Specifically, credit to micro and small industries grew by 8.9 per cent (reaching ₹7,98,473 crore), while medium industries grew by 18.5 per cent (reaching ₹3,63,245 crore) by March 2025.

Role of Non-Banking Financial Companies (NBFCs)

NBFCs are increasingly establishing their presence in the MSME sector by offering customized products and leveraging digital lending platforms. The proportion of MSME credit in the total credit extended by NBFCs reached nearly 10 per cent by end-March 2025. NBFCs recorded higher MSME credit growth compared to banks in certain segments, with their lending to MSMEs in the services sector accounting for a larger share than in the industrial sector.

Specialized Financing Mechanisms

The financial ecosystem has introduced several platforms to ease the liquidity constraints faced by MSMEs.

Trade Receivables Discounting System (TReDS)

TReDS is an electronic platform designed to facilitate the financing and discounting of trade receivables of MSMEs from corporates, Government departments, and public sector undertakings. This system gained further traction in 2024-25, with a sharp increase in the number and amount of invoices uploaded. The success rate, defined as the percentage of uploaded invoices that get financed, improved to 95.3 per cent in 2024-25 from 94.4 per cent the previous year.

Unified Lending Interface (ULI)

The ULI positions itself as a pivotal Digital Public Infrastructure (DPI) in the lending space. It allows lenders to connect to a broad array of data sources—such as land records, satellite services, and credit guarantees—to enable efficient credit assessments. As of late 2025, unsecured MSME loans were one of the 12 different loan journeys supported by the ULI platform.

Asset Quality and Soundness Indicators

Maintaining asset quality is essential for the sustained flow of credit to the MSME sector.

NPA Trends in Banks

The asset quality of priority sector advances (which include MSMEs) has improved since 2021-22, with the GNPA ratio declining to 4.0 per cent by end-March 2025. However, within the priority sector, Micro and Small Enterprises accounted for a significant share of NPAs. For example, in PSBs, the priority sector (including MSMEs) accounted for 72.6 per cent of their total NPAs, whereas in PVBs, it contributed 48.7 per cent.

NPA Trends in NBFCs

The NBFC sector witnessed broad-based improvements in asset quality, though sector-specific variations exist. For instance, GNPA ratios for Micro and Small industrial units in the NBFC sector stood at 5.4 per cent, while Medium industries were at 3.0 per cent as of March 2025.

Priority Sector Lending (PSL) Framework

MSMEs are a primary component of the Priority Sector Lending (PSL) requirements mandated by the RBI.

Targets and Achievements

Scheduled Commercial Banks have a sub-target of 7.5 per cent of Adjusted Net Bank Credit (ANBC) or CEOBSE for Micro Enterprises. By March 2025, SCBs collectively achieved an outstanding amount of ₹13,88,867 crore (9.2 per cent) for Micro Enterprises, exceeding the target.

Small Finance Banks (SFBs) and UCBs

The RBI revised PSL norms for SFBs, reducing the overall obligation from 75 per cent to 60 per cent of ANBC effective April 1, 2025. For Urban Co-operative Banks (UCBs), MSMEs held the largest share of total advances, at 36.5 per cent by March 2025. The share of credit to micro enterprises within UCBs increased, indicating an improved credit flow to smaller borrowers.

Regulatory and Supervisory Environment

Regulatory changes are designed to balance efficiency with stability while protecting small business interests.

Risk Weight Treatment

Under the draft directions for Basel III standards issued in October 2025, the RBI proposed granular risk weight treatment for exposures to MSMEs. This is intended to improve the resilience of the banking sector and align it with international best practices.

Interest Rates and Pre-payment Charges

Floating rate MSME loans are benchmarked to an external benchmark. Lenders are generally prohibited from charging pre-payment penalties on loans granted to Micro and Small Enterprises (MSEs) for business purposes, subject to certain threshold limits (e.g., loans up to ₹50 lakh for SFBs, RRBs, and NBFC-ML).

Collateral Flexibility

To offer greater flexibility to small borrowers, the RBI clarified in July 2025 that a voluntary pledge of gold and silver as collateral for MSME loans up to the collateral-free limit will not be considered a breach of guidelines.

Challenges and Future Outlook

While the sector remains robust, the sources indicate that banks and NBFCs must remain vigilant regarding emerging technological and cyber challenges. Furthermore, rapidly changing technology and digitalization are expected to change how MSMEs transact with banks, necessitating responsible technology adoption and strong risk management

{kind=link}