India to build 6,000 MTPA rare earth magnets capacity with ₹7,280 crore scheme for EVs, wind, defence.

Enhances India’s participation in global advanced-materials value chains while reducing import dependence and enabling long-term industrial growth.

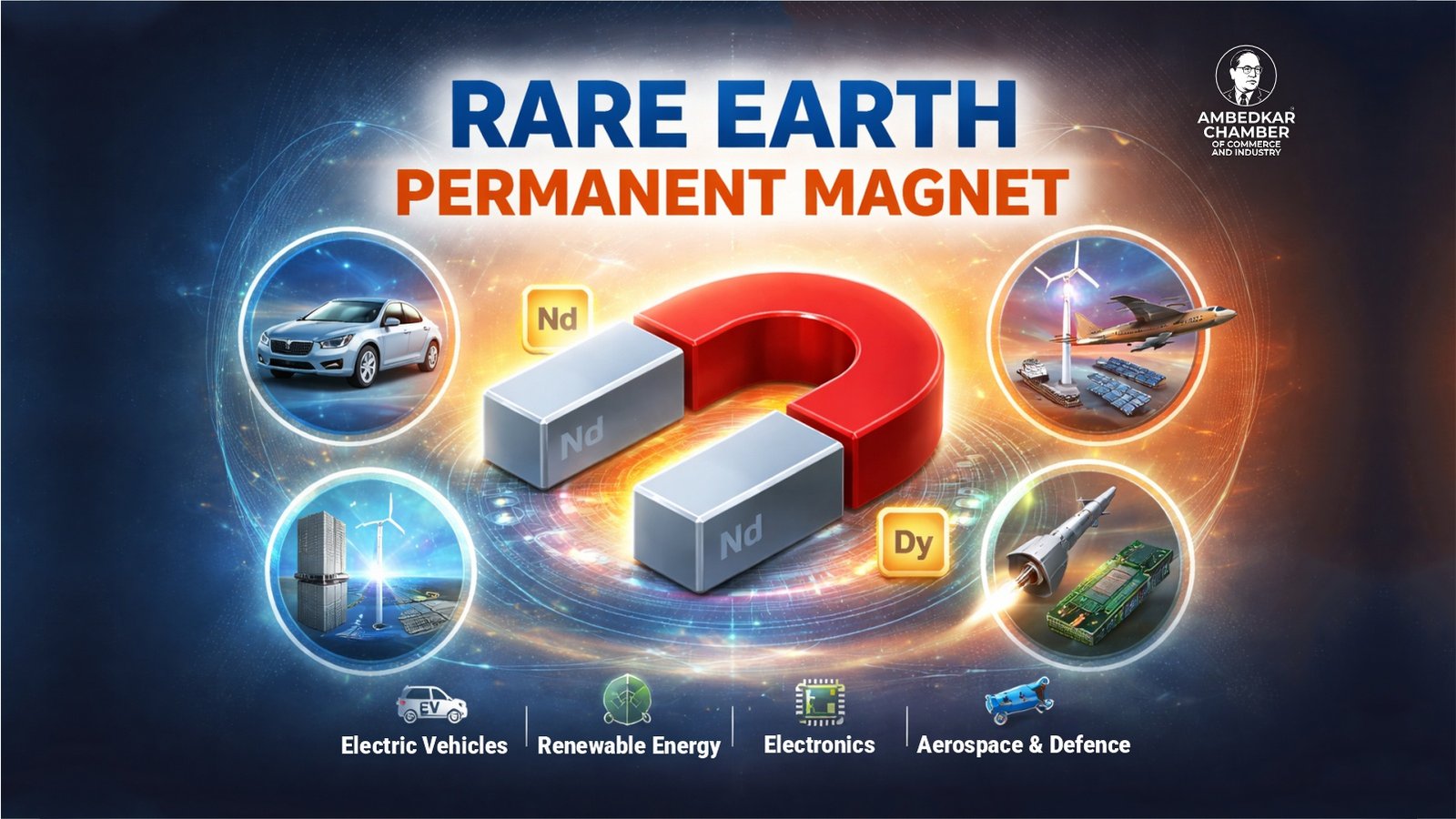

India is moving rapidly toward electric mobility, renewable energy expansion, advanced electronics manufacturing, and defence modernization. But one crucial input continues to expose a major strategic vulnerability—rare earth permanent magnets, which are essential for EV motors, wind turbines, and precision defence equipment.

To address this challenge, the Government has approved the ‘Scheme to Promote Manufacturing of Sintered Rare Earth Permanent Magnet’ with an outlay of ₹7,280 crore. The scheme aims to establish 6,000 metric tonnes per annum (MTPA) of integrated REPM manufacturing capacity in India, supporting the full chain—from rare-earth oxide feedstock to finished magnets.

The programme is a major step toward Atmanirbhar Bharat, while also aligning with India’s Net Zero 2070 goals by supporting technologies that drive energy efficiency and clean power systems.

By building a domestic integrated ecosystem, the initiative is intended to enhance self-reliance in a critical input for electric vehicles, renewable energy systems, electronics, aerospace and defence, and to position India as a key player in the global REPM market. It also supports broader national objectives, including Atmanirbhar Bharat, resilient supply chains for strategic sectors, and the country’s long-term Net Zero 2070 vision.

What is Rare Earth Permanent Magnet (REPM)?

REPMs are amongst the strongest types of permanent magnets and are used extensively in technologies requiring compact and high-performance magnetic components. Their high magnetic strength and stability make them integral to:

- Electric vehicle motors

- Wind turbine generators

- Consumer and industrial electronics

- Aerospace and defence systems

- Precision sensors and actuators

The ability of REPMs to deliver strong magnetic performance at small sizes makes them essential for advanced engineering applications. As India expands manufacturing across priority sectors such as clean energy, advanced mobility and defence, establishing a reliable domestic supply of high-performance magnets becomes increasingly important for long-term competitiveness and supply-chain resilience.

India’s Current Landscape and Need for the Scheme

India has a substantial base of rare-earth minerals, particularly monazite deposits located across several coastal and inland regions. These deposits contain about 13.15 million tonnes of monazite, holding an estimated 7.23 million tonnes of rare-earth oxides (REO), and occur in coastal beach sands, teri/red sands and inland alluvium in Andhra Pradesh, Odisha, Tamil Nadu, Kerala, West Bengal, Jharkhand, Gujarat and Maharashtra. These oxides serve as the primary raw material for downstream rare-earth industries, including permanent magnet manufacturing.

In addition, 1.29 million tonnes of in-situ REO resources have been identified in hard-rock areas of Gujarat and Rajasthan, while the Geological Survey of India has further augmented 482.6 million tonnes of rare-earth ore resources through extensive exploration initiatives. Together, these assessments demonstrate the availability of substantial raw material resources to support downstream rare-earth–based industries, including REPM manufacturing.

While India has a strong rare-earth resource base, domestic production of permanent magnets is still developing, and imports continue to meet a large part of current requirements. Official trade data indicates that India sourced a major share of its permanent magnet imports from China during 2022–23 to 2024–25, with import dependence ranging between 59.6% and 81.3% value-wise and 84.8% and 90.4% quantity-wise.

Meanwhile, forward demand projections highlight the need for enhanced domestic capability. India’s REPM consumption is expected to double by 2030, driven by growth in electric mobility, renewable energy deployment, electronics manufacturing and strategic applications. Developing integrated REPM manufacturing capacity is therefore essential to support rising domestic requirements and strengthen supply-chain resilience.

| Key Area | Short Facts |

|---|---|

| Monazite Deposits | India has 13.15 million tonnes of monazite deposits across coastal and inland regions. |

| Rare Earth Oxides (REO) Potential | These deposits hold about 7.23 million tonnes of rare-earth oxides (REO). |

| Major States | Deposits found in AP, Odisha, Tamil Nadu, Kerala, West Bengal, Jharkhand, Gujarat, Maharashtra. |

| Hard-Rock REO Resources | 1.29 million tonnes of in-situ REO identified in Gujarat and Rajasthan. |

| GSI Exploration Boost | GSI has added 482.6 million tonnes of rare-earth ore resources through exploration. |

| Import Dependence on China | China supplies most magnet imports (2022–23 to 2024–25): 59.6%–81.3% (value) and 84.8%–90.4% (quantity). |

| Demand Outlook | India’s REPM consumption is expected to double by 2030. |

| Key Demand Drivers | Growth in EVs, renewable energy, electronics, and strategic/defence applications. |

| Need for Domestic Capacity | Integrated REPM manufacturing is essential to reduce imports and improve supply-chain resilience. |

Core Elements of the Scheme

The scheme establishes a comprehensive framework for end-to-end REPM manufacturing in India, supporting both initial capacity creation and long-term competitiveness.

It aims to build a fully integrated production ecosystem for high-performance magnetic materials, creating 6,000 MTPA of domestic manufacturing capacity, from oxide feedstock to final product.

The total capacity will be distributed among up to five beneficiaries through a global competitive bidding process, with each beneficiary eligible for up to 1,200 MTPA, ensuring diversification along with adequate scale.

The scheme includes a strong incentive structure, with ₹6,450 crore earmarked as sales-linked incentives for REPM production over five years.

A ₹750 crore capital subsidy will support the establishment of advanced, integrated REPM manufacturing facilities.

The scheme will be implemented over seven years, comprising a two-year gestation period for setting up the integrated REPM facilities followed by five years of incentive disbursement linked to REPM sales. This structured timeline is intended to support timely capacity creation and provide stability during the initial production and market-development phase.

| Key Area | Short Facts |

|---|---|

| Scheme Purpose | Builds an end-to-end REPM manufacturing ecosystem in India for long-term competitiveness. |

| Capacity Target | Creates 6,000 MTPA integrated domestic REPM capacity (oxide to finished magnets). |

| Beneficiaries | Up to 5 beneficiaries selected via global competitive bidding. |

| Capacity per Beneficiary | Each beneficiary eligible for up to 1,200 MTPA capacity. |

| Sales-Linked Incentives | ₹6,450 crore incentives linked to REPM sales over 5 years. |

| Capital Subsidy | ₹750 crore capital subsidy for setting up integrated facilities. |

| Implementation Timeline | Total 7 years: 2 years setup + 5 years incentives linked to sales. |

| Expected Outcome | Supports timely capacity creation and stability during early production phase. |

National Priorities and Alignment with Broader Government Initiatives

The establishment of domestic REPM manufacturing capacity supports several national priorities, as these magnets are essential for strategic and high-technology sectors that are central to India’s industrial and technological advancement. The Governments’ initiative aims to strengthen domestic production, enhance supply-chain resilience for rapidly expanding industries while also contributing to India’s long-term sustainability goals.

Rare-earth magnets are widely used in energy-efficient motors, wind-power systems and other green technologies, and the initiative therefore aligns closely with the country’s broader clean-energy transition and its Net Zero 2070 vision.

Promoting domestic manufacturing of REPMs is equally relevant for national security and self-reliance. As these magnets are used in defence and aerospace systems, developing integrated production capability within the country contributes to secure access for critical applications and supports ongoing indigenization efforts.

This also complements India’s broader focus on strengthening its critical minerals value chain through the National Critical Minerals Mission (NCMM), which aims to improve availability and processing capabilities for key minerals, including rare-earth elements utilised across advanced sectors.

| Key Area | Short Facts |

|---|---|

| Purpose | Builds end-to-end REPM ecosystem in India. |

| Capacity | 6,000 MTPA integrated production (oxide to magnets). |

| Beneficiaries | Up to 5 companies through bidding. |

| Per Company Limit | Max 1,200 MTPA each. |

| Incentives | ₹6,450 crore sales-linked (5 years). |

| Capex Support | ₹750 crore capital subsidy. |

| Timeline | 7 years (2 setup + 5 incentives). |

| Outcome | Faster capacity build + early market stability. |

India’s End-to-End Value Chain Strategy

Critical minerals are a set of naturally occurring elements and compounds that have diverse irreplaceable industrial applications.

Given their central role in contemporary industrial economies, enabling technological advancements and boosting economies, access to critical minerals has become a strategic priority for India.

Approved in January 2025, the NCMM aims to secure a long-term sustainable supply of critical minerals and strengthen India’s critical mineral value chains encompassing all stages from mineral exploration and mining to beneficiation, processing, and recovery from end-of-life products.

These linkages demonstrate that developing domestic REPM manufacturing capability is not only a technological imperative but also a key component of India’s strategy to advance self-reliance, accelerate clean-energy adoption, support advanced mobility, and strengthen defence and strategic manufacturing ecosystems.

The REPM scheme further aligns with a wide set of ongoing government initiatives aimed at strengthening India’s critical mineral and advanced manufacturing ecosystem.

Policy reforms, particularly the amendments to the Mines and Minerals (Development and Regulation) Act, 1957, introduced a dedicated list of critical and strategic minerals and empowered the Government to auction mining leases and composite licences, enhancing opportunities for both private and public-sector participation.

| Key Area | Short Facts |

|---|---|

| Critical Minerals Meaning | Natural elements/compounds with irreplaceable industrial use. |

| Why It Matters | Essential for technology, industry growth and economic strength. |

| India’s Priority | Securing critical minerals is now a strategic national focus. |

| NCMM Approval | National Critical Minerals Mission approved in January 2025. |

| NCMM Goal | Ensures long-term supply and strengthens value chains end-to-end. |

| Value Chain Coverage | Exploration → mining → processing → recovery/recycling. |

| Link to REPM | Domestic REPM capability supports self-reliance and strategic sectors. |

| Alignment | REPM scheme aligns with India’s critical mineral and manufacturing push. |

| MMDR Reform Impact | Amendments enable critical minerals list + auctions for leases/licences. |

| Participation Boost | Opens stronger scope for private and public sector involvement. |

Mining Reforms for Critical Minerals

Mines and Minerals (Development and Regulation) Act, 1957 (MMDR Act) was enacted for regulation of mines and development of minerals. It has been reformed under the Mines and Minerals (Development and Regulation) Amendment Act, 2023 to strengthen India’s critical minerals ecosystem (for critical and deep-seated minerals) by opening private participation in all spheres of mineral exploration, empowering the Government to auction mineral concessions, and introducing a new exploration license regime.

Together, these initiatives, including the NCMM, regulatory reforms, and the REPM manufacturing scheme, create a strong domestic foundation for expanding REPM capacity and integrating it into India’s broader industrial, clean-energy and strategic priorities.

Global Context and India’s Opportunity

Global supply chains for rare-earth materials and permanent magnets have experienced periods of disruption, highlighting the importance of secure and diversified access to these resources. India has also undertaken several measures to support long-term supply security, including policy reforms and targeted domestic capability-building efforts.

The Ministry of Mines has entered into bilateral agreements with mineral-rich countries including Australia, Argentina, Zambia, Peru, Zimbabwe, Mozambique, Malawi and Côte d’Ivoire. India also participates in multilateral platforms such as the Minerals Security Partnership (MSP), the Indo-Pacific Economic Framework (IPEF) and the initiative on Critical and Emerging Technologies (iCET), which collectively support efforts to build resilient critical minerals supply chains.

Complementing these efforts, Khanij Bidesh India Limited (KABIL) is engaged in overseas exploration and acquisition of strategic mineral assets, including lithium and cobalt, through partnerships in countries such as Argentina. These initiatives form a key component of India’s strategy to secure critical minerals required for electric mobility, renewable energy systems, electronics and defence applications.

Khanij Bidesh India Limited (KABIL) is a joint venture of National Aluminium Company Ltd. (NALCO), Hindustan Copper Limited (HCL) and Mineral Exploration & Consultancy Limited (MECL) under the Ministry of Mines, established to secure India’s supply of critical and strategic minerals by identifying, exploring, acquiring and developing mineral assets overseas. Its mandate is to strengthen the domestic value chain for emerging technologies and clean-energy industries, giving a strong push to the Make in India initiative.

Against this backdrop, the development of domestic REPM manufacturing capacity offers India a timely opportunity to strengthen its position in global value chains for advanced materials while supporting industrial growth at home.

| Key Area | Short Facts |

|---|---|

| Global Supply Risk | Rare-earth and magnet supply chains face disruptions globally. |

| India’s Response | Focus on secure, diversified access + domestic capability building. |

| Bilateral Agreements | India signed deals with Australia, Argentina, Zambia, Peru, Zimbabwe, Mozambique, Malawi, Côte d’Ivoire. |

| Multilateral Platforms | Active in MSP, IPEF, and iCET for resilient supply chains. |

| KABIL Role | Secures critical minerals overseas through exploration and acquisitions. |

| Key Minerals Targeted | Focus on lithium, cobalt, and other strategic minerals. |

| KABIL Ownership | JV of NALCO, HCL, MECL under Ministry of Mines. |

| KABIL Mandate | Builds overseas mineral assets to strengthen domestic value chains. |

| India’s Opportunity | Domestic REPM capacity can boost India’s global advanced-materials position. |

| Industrial Impact | Supports EVs, renewables, electronics and defence growth in India. |

Conclusion

The Scheme to promote manufacturing of Sintered Rare Earth Permanent Magnets (REPM) is designed to enhance competitiveness, attract technology-driven investment and support long-term scalability. It also contributes to India’s energy-transition goals, given the role of these materials in high-efficiency systems. By establishing domestic capability and strengthening downstream linkages, this Government’s initiative will help generate employment, deepen industrial capacity and support the vision of Atmanirbhar Bharat and Viksit Bharat @2047.

{kind=link}