At the 26th UN Climate Change Conference (COP26), India committed to achieving net-zero emissions by 2070

India has an aspiration of becoming Viksit Bharat by 2047 and achieving USD 30 trillion economy. This economic expansion will be driven by a significant increase in industrial activity and accompanied by extensive infrastructure development. Increasing the share of manufacturing sector from 17% to 25% in GDP is a key national objective that is central to India’s developmental goals. India has also pledged to achieve net-zero greenhouse gas emissions by 2070. Therefore, a need was identified for developing industry specific green transition roadmaps that are consistent with Viksit Bharat by 2047. In this context, NITI Aayog in January 2026 released three reports on decarbonisation roadmaps for cement, aluminium and MSME sectors. These three reports have been prepared in consultation with line ministries/ departments, industry stakeholders, research institutions and knowledge partners.

At the 26th UN Climate Change Conference (COP26), India committed to achieving net-zero emissions by 2070, reducing carbon intensity by 45% by 2030, and increasing

non-fossil energy capacity to 500 GW by 2030. Achieving these ambitious targets will require significant efforts across all sectors, with industrial decarbonisation playing a

crucial role. Given the diversity of the industrial landscape, a sector-specific approach has been adopted as the pathway toward a green transition.

To enable a comprehensive strategy and develop tailored decarbonisation roadmaps, NITI Aayog has constituted a Technical Working Committee for the Micro, Small, and

Medium Enterprises (MSME) sector, comprising stakeholders from a wide range of backgrounds.

This report draws on the Committee’s work as well as extensive consultations with government agencies, industry associations, financial institutions, and technical

experts. It aims to present a practical, action-oriented roadmap focused on the key technological and financial interventions required to enable the MSME sector’s green

transition.

Suman Bery, Vice Chairperson, NITI Aayog observed that MSMEs are important members of domestic and international supply chains. He urged prioritizing technology adoption, access to affordable finance, skilling & regulatory reforms, and increased participation of female workforce to achieve overall competitiveness of MSMEs. B. V. R. Subrahmanyam, CEO, NITI Aayog emphasized that these roadmaps would serve as reference manuals for India to achieve its unique goal of becoming a developed country as well as decarbonising the industry simultaneously. S. C. L. Das, Secretary, MSME appreciated the broad focus of the reports and highlighted that cluster-based framework will help in effective implementation of the roadmap. Madhav Pai, CEO, WRI India recognized the timeliness of releasing these roadmaps in light of India’s developmental ambitions and climate commitments. Ishtiyaque Ahmed, Programme Director, NITI Aayog delivered a detailed presentation emphasizing that cement, aluminium and MSME sectors can be decarbonized using levers such as energy efficiency, round-the-clock renewables, CCUS and nuclear energy.

Roadmap for Green Transition of MSMEs

Released in January 2026, the NITI Aayog “Roadmap for Green Transition of MSMEs” is a 10-year strategic plan aiming to decarbonize India’s 63–69 million MSMEs through energy efficiency, green electricity adoption, and alternative fuels. It focuses on boosting competitiveness, lowering costs, and meeting net-zero goals, with a potential to mobilize ₹2 lakh crore in private investment.

The Roadmap for Green Transition of MSMEs focuses on three key levers:

- deployment of energy-efficient equipment,

- adoption of alternative fuels, and

- integration of green electricity.

The report also recommends the establishment of institutional mechanisms, governance structures, and a robust Monitoring, Reporting, and Verification (MRV) framework,

along with a dedicated Regulatory Impact Assessment (RIA) body. It seeks not only to chart comprehensive energy pathways for decarbonizing existing MSME units but also to ensure that new and upcoming MSMEs adopt low-carbon strategies from inception. Positioned at the intersection of global climate commitments, national development priorities, and local livelihood needs, MSMEs have the potential to emerge as both beneficiaries and key drivers of India’s sustainable industrial transformation.

The projected 69 million MSMEs in India are responsible for more than 45.73% of exports, 250 million jobs, 28.9% of the country’s GDP, and 25% of the energy used by the industrial sector (PIB 2021; TERI 2022; GoI 2023a).

Based on their annual turnovers and investments in plant and machinery, MSMEs have been classified into three categories as shown in Table 2 (GoI 2023b) (PIB 2025a).

A significant component of MSMEs is manufacturing, which employs more than 36 million people in India, and accounts for nearly 20 million units (Indusland Bank 2022) and represents an estimated 57% of all employment in the manufacturing sector, thereby having a significant societal influence.

Categorisation of MSMEs

| Classification | Manufacturing enterprises and enterprises rendering services |

|---|---|

| Micro | • Investment in plant and machinery or equipment not more than Rs. 2.5 crore and |

| Small | • Investment in plant and machinery or equipment not more than Rs. 25 crore and • Annual turnover not more than Rs. 10 crores |

| Medium | • Investment in plant and machinery or equipment not more than Rs. 125 crore and • Annual turnover not more than Rs. 500 crores • Annual turnover not more than Rs. 100 crores |

In India, MSMEs are commonly found in clusters. The clustering of units can be attributed to a variety of historical factors, including the accessibility of semi-skilled labour pools, the availability of fuels and raw materials, and the proximity of markets.

Around 17% of the (approximately 6,500 MSME) clusters are industrial clusters, and the remaining clusters are low-technology, micro-enterprise clusters (BEE 2010).

With at least 100 registered units in each, there are more than 140 clusters in India that are located inside or outside of metropolitan areas. The size of these urban clusters varies greatly; some clusters are so big that they produce 70-80% of a certain item produced in the entire nation.

The MSME sector is emissions and energy intensive. The issue is further made worse using antiquated machinery, such as furnaces, motors, boilers, etc., which consume more fuel than the average.

MSMEs also tend to use the cheapest locally available fuels to meet their industrial energy needs. These fuels may include coal, pet coke, and diesel, which produce high Green House Gas (GHG) emissions when burned.

Moreover, MSMEs depend heavily on electricity supplied by the grid. Furthermore, in 2022, 79% of the electricity produced was generated from fossil-fuel-based brown energy sources (CEA 2022), thus making the electricity grid predominantly brown.

All these factors make MSMEs a highly emission-intensive sector. GHG emissions for MSMEs are classified under three broad categories, Scope 1, Scope 2, and Scope 3:

Scope 1: Direct GHG emissions

Direct GHG emissions occur from sources that are owned or controlled by the MSME, for example, emissions from combustion in owned or controlled boilers, furnaces, vehicles, etc., emissions from chemical production in owned or controlled process equipment (USA National Grid 2024).

Scope 2: Indirect GHG Emissions from Purchased Energy

Scope 2 accounts for GHG emissions from the generation of purchased electricity, steam, heating, and cooling consumed by an MSME.

Purchased electricity is defined as electricity that is purchased or otherwise brought within the organisational boundary of the company.

Scope 2 emissions originate physically at the electricity generation facility.

Scope 3: Other Indirect GHG Emissions

Scope 3 is an optional reporting category that includes all other indirect emissions.

Scope 3 emissions are a consequence of activities of a business that occur from sources not owned or controlled by the company.

It includes indirect emissions, such as those from suppliers and the use of the organisation’s products. Emissions from external parties that procure, manufacture, and transport the raw materials and components used by businesses are considered upstream emissions.

Other upstream categories include emissions from waste generated and leased assets, employee commuting, and business travel. Emissions from the company’s product usage, transportation, and disposal fall under the downstream category (Jeremy Gregory 2024).

These upstream and downstream emissions are accounted for as Scope 3 emissions.

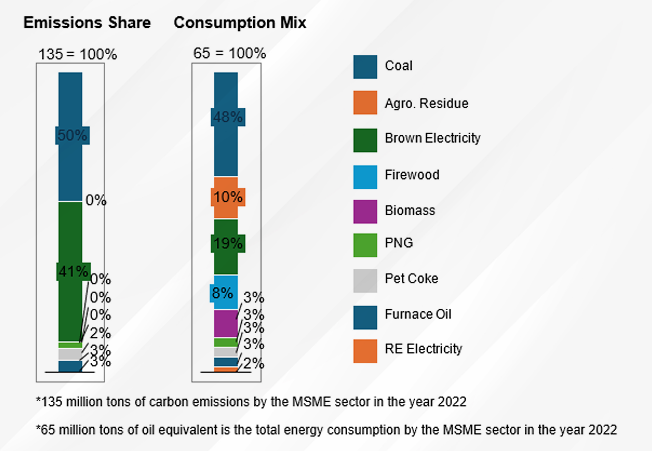

MSMEs, which largely form a part of the entire product value chain, are usually covered and reported under this category by large corporations. MSMEs emitted around 135 MtCO2e of carbon emissions in 2022.

Figure 3 illustrates the sectoral energy consumption among MSMEs with an emphasis on the Specific Energy Consumption (SEC) for each of the five sub-sectors paper, textiles, steel rerolling, foundry and forging.

These subsectors alone account for more than 60% of the total MSME emissions. Coal and electricity, which together comprise approximately 54 percent of the fuel mix, are responsible for around 90% of the overall emissions. The details of the calculations have been presented as Annexure 2.

Figure 4 illustrates the fuel composition and contributing emission intensities of the top five emission-intensive MSME sub-sectors.

The complete calculation methodology is outlined in Annexure 3.

Need for a Green Transition

India presented its long-term plan to reach 500 GW of renewable energy (RE) capacity by 2030 and net-zero emissions by 2070 at the 27th Conference of the Parties (COP27) to the United Nations Framework Convention on Climate Change (UNFCCC 2022).

To meet these climate targets, emission reduction and renewable energy expansion will be necessary across all economic sectors, including MSMEs. Encouraging MSMEs to implement decarbonisation measures is critical for achieving the Sustainable Development Goals (SDGs), particularly SDG 9 (infrastructure, industry, and innovation), SDG 12 (responsible production and consumption), and SDG 13 (climate action).

This climate transition risk is becoming evident for MSMEs and thus warrants the government’s immediate attention.

MSMEs stand to gain several advantages through the green transition, including:

| Reason | Benefit / Impact |

|---|---|

| Access to Global Markets | Enables participation in global supply chains that demand cleaner production |

| Access to Better Technology | Increases productivity and efficiency through adoption of modern, cleaner machinery |

| Economic Benefits | Leads to long-term cost savings via reduced energy bills, improved competitiveness, and access to green finance |

| Compliance with Standards (CBAM, BRSR, Eco Mark) | Helps avoid penalties, retain export eligibility, and meet ESG reporting norms increasingly expected by regulators and buyers |

Building Climate Resilience

Climate change phenomena are often viewed as macro-level environmental effects, such as rising temperatures or changing rainfall patterns. Addressing these impacts of climate change is a key challenge of this century for governments, communities, and businesses alike.

The consequences of climate change, including more frequent and intense floods, are already affecting Indian MSMEs, even if they are not explicitly recognised as climate-related disruptions.

The reasons why Indian MSMEs are particularly affected by climate change impacts are manifold, and some are due to their inherent challenges, like financial resources and access to credit. Climate change and associated hazards severely impair MSMEs, disrupting not only their daily operations but also the entire value chain.

These enterprises face vast and multi-faceted risks, from fluctuating costs and delayed deliveries to unpredictable material availability, along with shutdowns caused by floods and degraded infrastructure.

This is more pertinent for the MSMEs operating on low technology levels, as they are more severely affected by climate change than high-tech businesses and have fewer resources to cope with the impacts (WRI India 2024; GiZ India 2024).

Given these risks, MSMEs must adapt and build resilience across the board. Climate adaptation is critical for their long-term competitiveness and survival. This could be a win-win situation, with several benefits such as risk reduction and increased resilience, cost savings, promotion of innovation, and gaining a competitive advantage.

Given these global changes, it is very important to have a coherent framework and program, which can guide the industry and MSMEs over the next 10-15 years in tackling climate change, which is directly impacting policies, regulations, business models, supply chains, and global trade patterns.

Impact of Cyclones and Heat Stress/Heat Waves on MSMEs in India

Cyclone Michaung hit Tamil Nadu in December 2023, affecting 4,800 MSME units across 24 industrial estates. This resulted in losses of at least USD 360 million. Heavy rainfall in 2022 disrupted goods movement and factory production, costing Gujarat industries approximately USD 600 million.

Similarly, the Chennai floods (2015), Kerala floods (2018), and Cyclone Fani in Odisha (2019)— all caused significant losses among MSMEs, ranging from several hundred crore to tens of thousands of affected units. Between 2001 and 2020, India lost approximately 259 billion hours of labour or $624 billion (Rs 46 lakh crore) annually because of heat and humidity.

According to an International Labour Organisation (ILO) 2019 report, by 2030, India could account for 34 million of the projected 80 million global job losses due to heat stress-related productivity decline. Humidity is also likely to cause inventory damage, machinery malfunctions, equipment rusting, and an increased cooling demand.

Furthermore, increased heat raises the risk of industrial fire outbreaks and chemical hazards in manufacturing facilities.

Achieving Profitability through Advanced Technology

Implementing green transition technologies can help MSMEs reduce costs and become more competitive. Adopting cleaner fuels like biomass, biofuels, biogas, and RE sources reduces emission intensity and expands access to low-emission product markets.

Transitioning to lower emission-intensive fuels like Liquefied Petroleum Gas (LPG) and Piped Natural Gas (PNG) can be a crucial first step in reducing emissions, since MSMEs are heavily reliant on energy-intensive fuels like coal.

Multiple incentives are also available to implement energy-efficient technologies, such as accelerated depreciation and credit-linked subsidy schemes for business expansion.

MSMEs adopting greener technologies have payback periods ranging between 1-5 years. Furthermore, adopting green electricity and alternate fuels not only reduces emissions but also decreases dependency on grid electricity and traditional emission-intensive fuels like diesel, which are used in generator sets.

These significant savings can increase MSME profitability, support business expansion, generate employment, and reduce emissions. Research indicates that the willingness to purchase sustainable products at a premium is more prevalent in developing nations like India, Indonesia, Brazil, and China than in developed economies.

Given the momentum from international guidelines and regional measures mandating a reduction in emissions and adoption of sustainability, MSMEs must prioritize cost savings and advance towards decarbonisation.

Adhering to International Standards and Regulations

Ensuring economic competitiveness of the MSME sector in an era of globalisation is crucial. Adopting clean energy measures can play a vital role in strengthening the market position of MSMEs.

A critical development is the Carbon Border Adjustment Mechanism (CBAM), a policy introduced by the European Union (EU) to impose carbon pricing on certain carbon-intensive products imported into the region (European Union 2023).

After a three-year transition phase, CBAM is expected to take effect in January 2026, with the possibility of expanding its scope to other high-emitting industries and indirect emissions. This policy aims to prevent “carbon leakage,” where companies relocate production to countries with less stringent carbon regulations.

This will significantly impact Indian MSMEs as Indian MSME segments contribute largely to the total exports of textiles, steel, paper, and pulp for handicraft (around 40 percent), and engineered goods (over 60 percent).

Indian products have significantly higher carbon intensity than the EU and many other countries because coal dominates the overall energy consumption (The Times of India 2023). MSMEs will face increased costs for EU exports due to CBAM purchase certificates tied to product carbon emissions.

Additionally, an increase in the administrative burden can be expected as CBAM involves monitoring, reporting, and verifying emissions, which can be particularly challenging for smaller businesses like MSMEs. Apart from the EU, other countries such as the UK, Canada, and Japan have also been considering similar mechanisms. Such measures could severely impact Indian MSME export prospects.

Fuel Consumption in the Top 5 MSME Subsectors and Resultant Emissions (2022)

- Total MSME energy consumption in year 2022 – 65 (MtOe)

- Total MSME emissions in year 2022 – 135 Mt

- Fuel wise consumption for 5 MSME subsectors provided in Annexure 2

| Fuel Type | Energy Consumption Units (MtOe) (Derived from BEE Reports) | Energy Consumption (%) | Resultant Emissions (Mt) | Resultant Emissions (%) |

|---|---|---|---|---|

| Coal | 9.6 | 48 | 43.6 | 50 |

| Agro Residue | 2.0 | 10 | 0 | 0 |

| Firewood | 1.7 | 8 | 0 | 0 |

| PNG | 0.6 | 3 | 1.6 | 2 |

| Pet coke | 0.7 | 3 | 2.7 | 3 |

| Biomass | 0.7 | 3 | 0 | 0 |

| Furnace Oil | 0.6 | 3 | 2.9 | 3 |

| Electricity (Grid) | 3.8 | 19 | 35.7 | 41 |

| Electricity (RE) | 0.3 | 2 | 0 | 0 |

| Total | 20 | 86.5 |

On the domestic front, Business Responsibility and Sustainability Reporting (BRSR) represents India’s first framework mandating the provision of quantitative sustainability metrics from Indian companies (the top 1,000 NSE-listed companies by market capitalisation) (SEBI 2023).

The new BRSR framework, created by the SEBI, oversees the country’s securities markets. It was inspired by the Business Responsibility Report (BRR 2012) published by the Ministry of Corporate Affairs.

The new BRSR works with other globally recognised reporting frameworks, including the Task Force on Climate-Related Financial Disclosures (TCFD), the Sustainability Accounting Standards Board (SASB), and the Global Reporting Initiative (GRI).

Respect for the environment and efforts to preserve and repair it are among the guiding principles of this framework, under which 51% of India’s top 100 listed companies voluntarily reported Scope 3 emissions. As large corporations report on these emissions, MSMEs serving as upstream and downstream partners in the entire value chain will face compliance obligations.

Only 2-3 % of manufacturing MSMEs sell directly to retail customers, while more than 90% sell through traders and other upstream manufacturers; hence, they may soon be asked to reduce their carbon footprint.

This necessitates the reduction of carbon emissions for MSMEs as regional practices aim towards sustainability. Additionally, other sustainability measures, specifically the Ecomark rules by MoEFCC, will benefit MSMEs in the long run.

Reduction in MSME Emissions (2022)

- Total MSME emissions in year 2022 = 135 Mt

- Top 5 MSME sub sectoral emissions in 2022 = 86.5 Mt

- MSME Emissions due to Other Sectors except the 5 listed = 48.5 Mt

| MSME Subsector | Energy Efficiency Potential (%) (derived from EE initiatives mentioned in BEE reports) | Sectoral Emissions (Before energy efficiency interventions) (Mt) | Sectoral Emissions after application of energy efficiency (Mt) |

|---|---|---|---|

| Textile | 60 | 24.7 | 9.9 |

| Paper and Pulp | 7 | 30.3 | 28.1 |

| Foundry | 21 | 9.7 | 8.6 |

| Forging | 22 | 9.6 | 7.5 |

| Steel Rerolling | 12 | 12.4 | 9.6 |

| Total | 86.5 | 63.6 |

Ecomark Rules 2024

On 26th September 2024, the MoEFCC notified the Ecomark Rules, 2024 to label products that have a lesser adverse impact on the environment.

The Ecomark will be granted to a product if it holds a license or a certificate of conformity to Indian Standards issued under the Bureau of Indian Standards Act, 2016, or the Quality Control Orders issued by the Central Government.

Other criteria that may be considered for the grant of Ecomark include reduction of pollution by minimising or eliminating the generation of waste and environmental emissions; recyclability or recycled material or both; reduced use of non-renewable resources, including non-renewable energy sources and natural resources; reduced use of any material, which has adverse impacts on the environment.

Any Ecomark, when granted, is valid for 3 years or until there is a change in the Ecomark criteria for the product.

These rules imply that the use of environment-friendly ‘green’ products will be promoted among consumers and will be the preferred choice for producing final goods.

MSMEs that are responsible for final product preparation and delivery will be benefited with Ecomark label on their products.

MSMEs Need Additional Support for Green Transition

Implementing measures that aim to reduce the Scope 1 and Scope 2 emissions of MSMEs is essential.

The enhancement of energy efficiency and the adoption of green electricity and alternate fuels can be the key drivers for this transition. Despite the economic benefits and compliance with international standards, the adoption of clean energy interventions is low due to a multitude of reasons.

Due to their limited manpower and inclination to focus on production and marketing processes, MSMEs are left with little capacity to adopt clean energy solutions. They require support from external entities for the adoption of clean energy solutions, including access to cutting-edge innovations, technical know-how, and best practices.

MSMEs face a range of challenges in areas such as energy efficiency, green electricity adoption, and the use of alternate fuels, including the following:

Challenges in Green Transition for MSMEs

| Category | Key Challenges |

|---|---|

| Energy Efficiency (EE) | • Lack of trust in the ecosystem: MSMEs fail to collaborate with Energy Service Company (ESCO) despite performance guarantees due to lack of trust/understanding of such mechanism. • Awareness and capacity to implement latest technology: MSMEs are unaware of the technologies and performance guarantee models run by energy services companies. |

| Green Electricity (GE) | • Perceived risk of payment default by MSMEs: RESCOs require risk of extending services to MSMEs to be mitigated due to perceived payment defaults. • Stakeholder support: State Distribution Companies (DISCOMs) are required to extend timely support to the ecosystem to get such renewable power plants online. |

| Alternative Fuels (AF) | • Awareness on various agro feed: MSMEs are typically unaware of the possible agro residues that can be made into brickettes and pellets for biomass firing. • Scalability issues: Many biofuels and products are perishable and thus have lower shelf life making it logistically challenging. Further, seasonality factors impact availability and may potentially lead to fuel shortage. |

Other issues faced by MSMEs include

i. Budget constraints

MSMEs often operate within tighter budgets and have limited access to capital compared to larger enterprises, which makes them more vulnerable to cost fluctuations. These enterprises often face a high cost of compliance that consumes a significant portion of their resources.

Furthermore, MSMEs usually compete with larger firms that benefit from economies of scale, making it challenging to maintain competitive pricing for their finished goods, all of which contributes greatly towards their cost sensitivity. MSMEs in Energy Service Company (ESCO) markets often prefer cheaper alternatives (usually low quality) to ESCOs’ solutions that tend to reduce the scale of impact intended.

ii. Access to finance

The Government has been supporting MSMEs by providing finance to upgrade machinery, infrastructure, and cluster-related developmental projects across India. Although public finance and grants from the Government and philanthropic organisations enable initial adoption of clean energy technologies, access to finance from mainstream private and public sector banks is necessary to achieve scale.

However, access to such financing is limited due to the high perceived risk in lending to MSMEs, high transaction costs to service these low-value loans, low credit rating/scoring of MSMEs, low business visibility, and the lack of understanding of clean energy technologies.

Even when financing options are available, MSMEs find them unviable and unattractive as they are often expensive, involving a cumbersome documentation process requiring additional collateral security to cover risks.

iii. Cash-flow management challenges

MSMEs face hurdles in cash flow management, which heavily impact their product delivery, operations, and overall functioning. Some of these are due to late payments from customers, inefficient invoicing and seasonal fluctuations in product demand patterns. A significant amount is usually tied as receivables, which restricts working capital, thus limiting funds for expansion or immediate needs.

(Source: Roadmap for Green Transition of MSMEs)

{kind=link}